BusinessiOS7 Mins reading

Passkeys: Why the future of login doesn't involve passwords

Andrej Jaššo26 Feb 2026

Insurance companies are moving beyond viewing mobile interfaces merely as repositories for policies and are transforming them into smart platforms that manage health, property, and finances in real time. This analysis, based on the market expertise of the GoodRequest agency, combines a business perspective with the real-world needs of digital service users.

Digital transformation isn’t just about converting paper documents into digital formats. Its goal is to create services that make the insurance company a useful partner in everyday life.

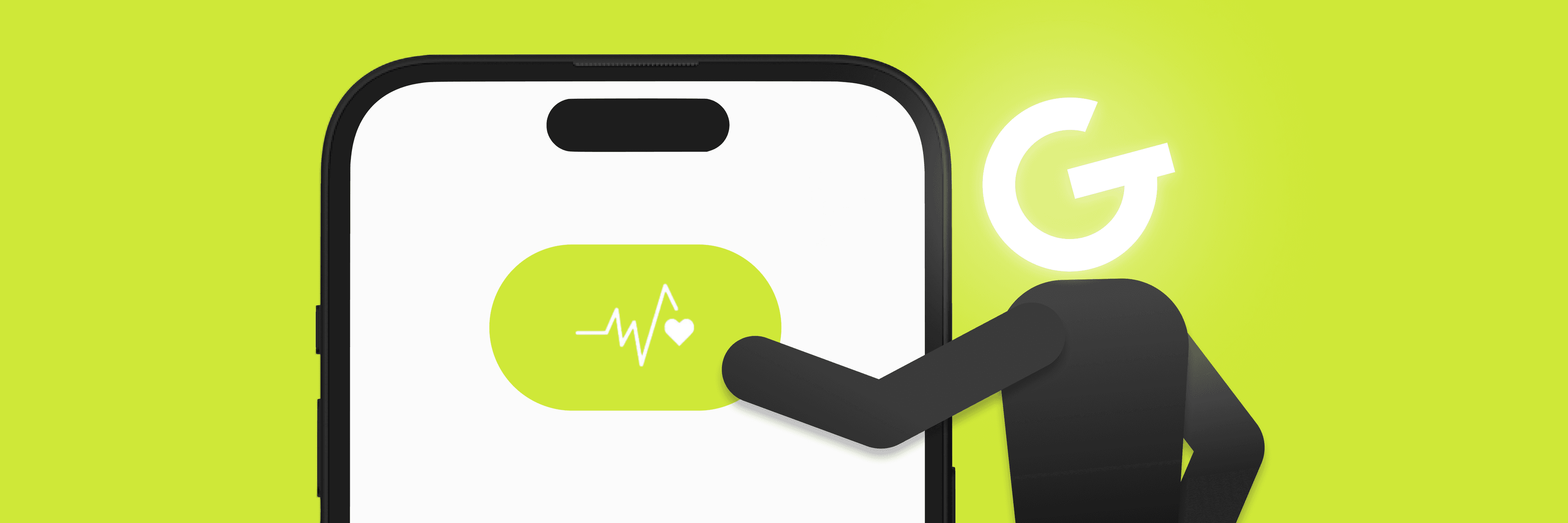

The app is becoming the digital hub of life, where clients can manage both their health and assets in one place. Abroad, it is common to expand this space to include value-added services.

Global investment in AI-powered technologies grew by 40% in Q2 2024. Artificial intelligence is evolving from a futuristic concept into a tool that significantly accelerates processes.

The future of insurance is moving toward promoting health and preventing losses.

Even the most advanced technology won’t help if users encounter barriers that frustrate them and drive them to visit a branch in person.

A high-quality digital experience requires an understanding of each group’s lifestyle and financial background.

Companies considered technology leaders achieve up to 37% higher revenue. For 2026, we identify the following six pillars as key technological challenges:

💡 Prevention tip: Motivate users to be responsible before damage occurs. Reward them for safe drivingor regular preventive health care.

Between 2026 and 2030, we expect pressure to grow in the insurance market to provide the best possible digital experience. Simplicity, functionality, self-service, and assistance will become the standard. An advanced experience includes the integration of AI into everyday use, a rewards system for loyal customers, and gamification.

However, it is essential to remember that an app is not a product, but a channel. Even the best digital experience cannot compensate for a subpar core service – such as an unfavorable offer, slow claims processing, or misleading communication. Insurance companies must not view the app merely as a "quick win", but as a tool for building long-term relationships and customer loyalty. Those who fail to offer attractive insurance and remain stuck in low levels of digitization and complex processes will be left behind.